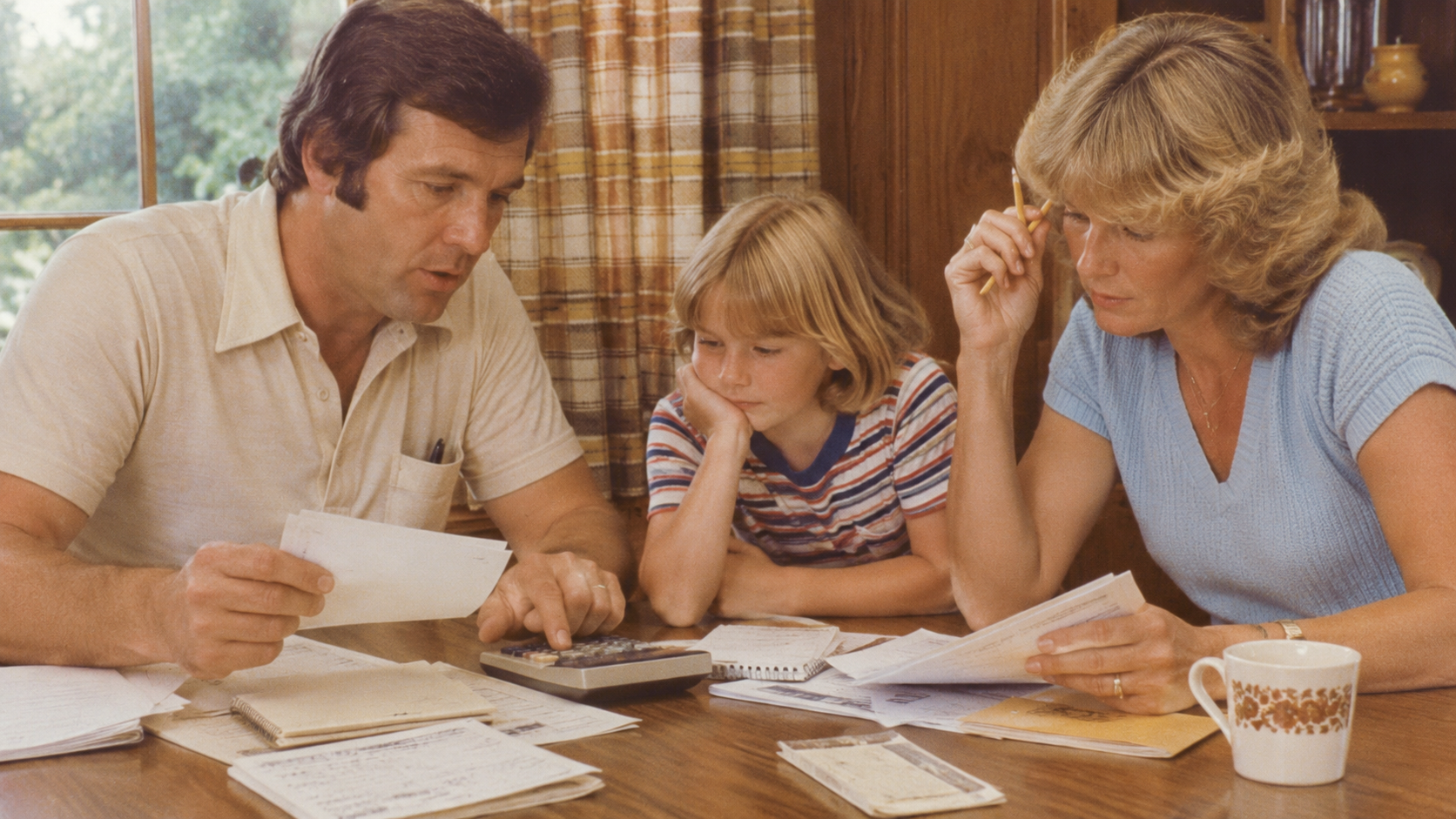

If you grew up in the 70s or 80s, you watched a lot of financial stuff happen at the kitchen table.

The checkbook coming out on Sunday nights. The long patient phone call to argue down a charge on the cable bill. Cash envelopes in a kitchen drawer, marked for groceries, Christmas, or the car. Parents complaining about the price of gas. A receipt drawer that nobody opened until tax time.

Nobody sat us down and said do this. We just saw it, week after week, year after year, and picked it up the way you pick up an accent. Research on how kids learn financial habits has found that most of it happens by observation — kids absorbing how the adults around them handle money way before anyone tries to explain it.

But the world that produced those habits has mostly moved on. Younger adults grew up in a different house, financially speaking — one with apps where there used to be checkbooks, and one-click checkout where there used to be a drive to the store.

What we ended up with, instead, is a set of instincts about money — ten of them below.

1. Knowing your bank balance from memory rather than checking an app

Before banking apps, you knew what was in your checking account because you had to.

Bounced checks cost real money — overdraft fees that mattered when fees that small mattered, and the social cost of having the grocery store run your check back through. Our parents kept a running figure in their head and reconciled it weekly against the paper statement.

We watched them do it, and somewhere along the way we picked up the same habit — a rough number in our head at all times, accurate within a few dollars. We’ll still check the app, but the app is confirming what we already know.

2. The instinct to call and negotiate a bill rather than just paying it

Our parents called the phone company. They called the cable company. They called the hospital. They called and asked, plainly, whether the charge was right and whether anything could be done about it, and a startling amount of the time, something could.

The bill was a first draft, not a final number. We watched this happen at the kitchen table over and over — the long hold, the patient escalation to a supervisor, the small triumph of getting a fee removed — and we absorbed the basic premise that prices on a piece of paper are often negotiable.

More Bolde Stories

3. Keeping a physical cash envelope for specific expenses

Maybe it was the grocery envelope. Maybe it was the Christmas envelope, slowly filling up from August on.

The principle was the same — money for a specific purpose lived in a specific place, and when the envelope was empty, that thing was done for the month. This was a visible fact of how a household worked, and even those of us who don’t literally use cash envelopes anymore have a digital version of the same instinct — separate accounts, sub-accounts, a mental ringfence around money that’s already been assigned a job.

4. Treating a credit card balance as an emergency

For our parents, carrying a credit card balance meant something had gone wrong.

A car needed a transmission, somebody had been to the ER, the furnace had died in February. A balance was a sign that the regular system had failed, and you were now in repair mode until you paid it back down.

The idea of just carrying a few thousand dollars on a card indefinitely — paying the minimum, treating it as background noise — would have struck them as a slow-motion emergency. We inherited the unease.

5. The reflex to do a small home repair yourself before calling someone

The plumber was an expense, the handyman was an expense, the appliance repair guy was an expense, and all three were called only after our parents had genuinely tried to fix the thing themselves. Out came the toolbox, out came the manual, out came the long-suffering call to a cousin who knew about furnaces.

We saw a thousand minor repairs happen— the running toilet, the squeaky door, the dishwasher that wouldn’t drain — and we absorbed the default order of operations.

Try it yourself first. Watch a video. Ask someone who knows. Call the professional last, when you actually need them.

The instinct survives even when YouTube has made it ten times easier than it was for our parents.

More Bolde Stories

6. Buying durable items once rather than cheap items repeatedly

Our parents bought a vacuum cleaner that lasted twenty years.

They bought a winter coat and wore it for a decade.

The logic was specific and explicit — the cheap version costs less today and more over time, because you’d buy it three times. The durable version costs more today and was the last one you’d buy.

We absorbed this as a default approach to purchases that matter, and it sits awkwardly now in a world where most consumer goods aren’t really built to last twenty years anymore, regardless of what you pay for them.

7. The discomfort of carrying debt that isn’t a mortgage

A mortgage was respectable debt — you got something for it, and the house was worth more than the loan.

Almost everything else made our parents uncomfortable.

Car loans were tolerated but disliked. Student loans were a concession to necessity. Credit card balances, see item four.

The category of debt I am carrying for ordinary life was meant to be very small or empty, and if it crept up, the family’s attention turned to bringing it back down. Most of us still have that orientation — a low-grade itch about non-mortgage debt that doesn’t really go away until the balance does, regardless of what the interest rate technically allows.

8. Knowing the price of staples without looking

Our parents knew what a gallon of milk cost.

They knew what a dozen eggs cost.

They knew what a gallon of gas cost, and they knew when it had gone up.

They weren’t tracking prices on a spreadsheet — they bought these things every week, paid attention to what they paid, and noticed when the number moved. We picked up the habit by osmosis. Most of us still walk into a grocery store with a rough mental price list, and we can tell when a store is overcharging on basics.

The number isn’t always precise. But it’s there, and it updates on its own, the same way our parents’ did.

More Bolde Stories

9. Keeping receipts just in case

The receipt drawer. The receipt envelope in the file cabinet. The shoebox of receipts in the closet, kept until tax time and then partly kept after that anyway.

Receipts mattered because returns required them, warranties required them, expense reports required them, and the strange charge on the credit card statement at the end of the month could only be disputed if you had the paper. There was no digital trail of anything you bought — if you didn’t have the receipt, the purchase essentially hadn’t happened, at least not in a way you could prove.

We saw that drawer fill up, and most of us still keep some version of it, even though half the proof we’d need now is in an email somewhere. The habit is older than the reason for it.

10. The habit of waiting overnight before making any purchase over a certain amount

Our parents didn’t buy big things on impulse. The new couch, the new washer, the new winter tires — those decisions sat overnight, sometimes for a week, while they thought about it, compared prices, and asked around.

Sometimes the thing was bought, sometimes it wasn’t, but the gap was never zero.

For most of us, there’s still a number above which a purchase has to sleep on a shelf overnight before it can happen, and the number rises with income but the rule doesn’t go away. The instinct is older than any of the math we’d use to defend it.